Choosing the right auto insurance policy isn’t just about meeting legal requirements—it’s about protecting your finances in real-world scenarios that basic coverage often overlooks. I’ve reviewed dozens of policies and claims cases, and one pattern stands out: the difference between a stressful loss and a manageable inconvenience often comes down to the add-ons you choose. While insurers market these extras aggressively, not all of them deliver meaningful value. Some are essential depending on your driving habits, vehicle type, and financial situation, while others are redundant or overpriced.

In this guide, I break down 10 of the most common auto insurance add-ons, explaining exactly what they cover, when they’re worth it, and when you can skip them. I’ll also point out how these extras interact with broader insurance strategies, such as those discussed in auto add-ons and risk management principles used across policies like utility contractor coverage. Whether you’re optimizing for cost savings or maximum protection, this article will help you make smarter, data-backed decisions.

Get the #1 Wireless Door Camera

REOLINK Bestseller: 2K Weatherproof Video Doorbell, No Monthly Fees.

1. Gap Insurance (Guaranteed Asset Protection)

Gap insurance covers the difference between your car’s depreciated value and the remaining loan balance if it’s totaled. This is critical for new vehicles, which lose up to 20% of their value in the first year.

I recommend this add-on if you financed your car with a low down payment or long-term loan. For example, drivers exploring options like hyundai gap often benefit the most.

Verdict

Worth it for financed or leased vehicles; unnecessary if you own your car outright.

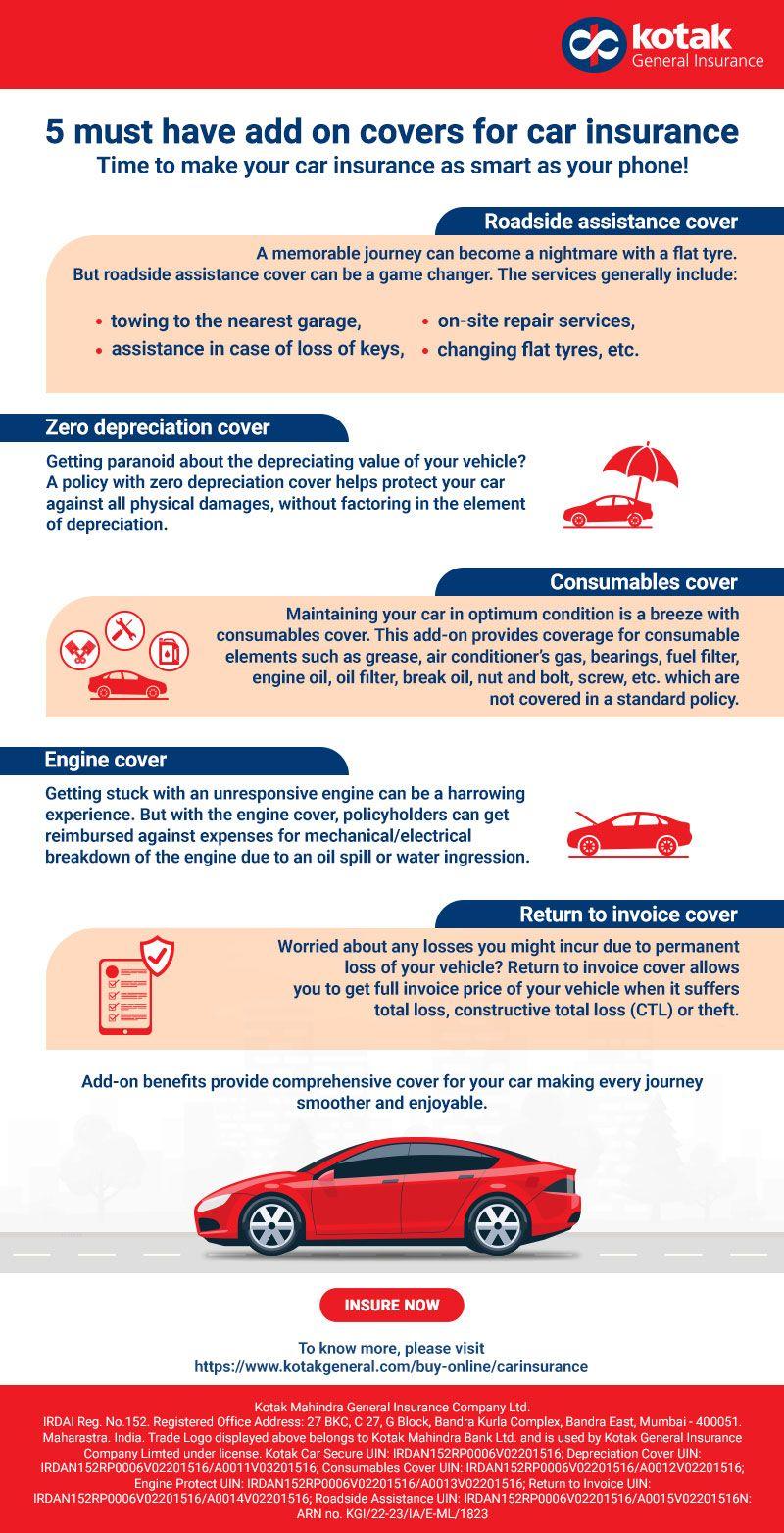

2. Roadside Assistance

This add-on covers towing, battery jumps, fuel delivery, and lockout services. While convenient, it often duplicates services offered by auto clubs or even credit cards.

I’ve found that standalone providers frequently offer better coverage and faster response times.

Verdict

Situational—worth it if you don’t already have coverage elsewhere.

3. Rental Car Reimbursement

This covers the cost of a rental vehicle while your car is being repaired after a covered claim. Daily limits typically range from $30 to $50.

For commuters or those without a backup vehicle, this is a practical safeguard. It’s particularly useful in scenarios discussed in claim without police report situations where delays can occur.

Verdict

Worth it for daily drivers; optional if you have alternative transportation.

4. New Car Replacement

This upgrade replaces your totaled vehicle with a brand-new model of the same make, rather than paying depreciated value.

I’ve seen this add-on provide thousands in additional value during claims, especially within the first two years of ownership.

Verdict

Highly recommended for new vehicles.

5. Accident Forgiveness

This prevents your premium from increasing after your first at-fault accident. While appealing, insurers often charge higher upfront premiums for this feature.

In many cases, the cost outweighs the benefit unless you’re a high-risk driver.

Verdict

Not always worth it—analyze cost vs. potential premium increase.

6. Comprehensive Coverage Enhancements

Standard comprehensive insurance covers theft, vandalism, and natural disasters, but add-ons may expand coverage to include glass repair or lower deductibles.

This becomes valuable in areas prone to weather-related damage, similar to risks covered in roof hail damage claim scenarios.

Verdict

Worth it in high-risk regions.

7. Personal Injury Protection (PIP) Upgrades

PIP covers medical expenses regardless of fault. Enhanced versions may include lost wages and rehabilitation costs.

I consider this essential for drivers without robust health insurance. It aligns with broader protection strategies seen in policies like balanced care.

Verdict

Strongly recommended if health coverage is limited.

8. OEM Parts Coverage

This ensures repairs use original manufacturer parts instead of cheaper aftermarket alternatives.

For newer or high-value vehicles, this preserves resale value and performance integrity.

Verdict

Worth it for newer cars; less critical for older vehicles.

9. Vanishing Deductible

This reduces your deductible over time for safe driving. While appealing, the savings often take years to materialize.

I’ve found that drivers rarely benefit unless they maintain a long claim-free history.

Verdict

Low priority for most drivers.

10. Ride-Sharing Coverage

If you drive for Uber or Lyft, personal policies typically exclude coverage during commercial use. This add-on fills that gap.

It’s essential for gig economy drivers and complements liability considerations similar to riggers liability or fort worth landlord protections.

Verdict

Essential for ride-share drivers.

How to Decide Which Add-Ons You Need

When evaluating add-ons, I focus on three key factors:

- Vehicle value: Newer cars justify more protection, including gap and OEM coverage.

- Financial risk tolerance: If you can’t easily absorb a loss, add-ons provide critical protection.

- Driving habits: High-mileage or urban drivers benefit more from extras like rental reimbursement.

It’s also important to avoid overlapping coverage. For example, roadside assistance may already be included in memberships or credit cards, similar to how overlapping benefits can occur in policies like trulife or innovative group.

Common Mistakes to Avoid

Overinsuring Older Vehicles

If your car’s value is low, expensive add-ons may not make financial sense. In these cases, liability-only coverage may be sufficient.

Ignoring Policy Details

Not all add-ons are created equal. Coverage limits, exclusions, and claim processes vary widely between insurers like those discussed in advantage 1 auto or comer agency.

Failing to Compare Providers

Pricing for add-ons can differ significantly. Always compare multiple insurers, including niche providers such as el segurito or ezee.

Are Auto Insurance Add-Ons Worth It Overall?

In my experience, the right add-ons can dramatically improve your financial protection, but only when chosen strategically. Gap insurance, rental reimbursement, and ride-sharing coverage consistently deliver strong value. On the other hand, features like vanishing deductibles or accident forgiveness often provide limited returns.

The key is alignment—matching your coverage to your actual risk exposure. This is the same principle used across insurance categories, from auto to specialized policies like abbey or compliance-focused areas such as csr.

Ultimately, smart drivers don’t just buy insurance—they optimize it. By carefully selecting the add-ons that truly matter, you can reduce out-of-pocket costs, avoid coverage gaps, and gain peace of mind every time you get behind the wheel.

Home Decor Shop

Acacia frida deluxe solid wood bed frame |

Bedroom bench |

Bed chest drawers |

Lingerie dresser |

Frame base |

Mirror with jewelry storage |

30 Bathroom Vanity |

Memory foam queen mattress |

Mattresses for back pain |

Nightstand set of 2 |

Grand Goldman Shop |

Civil Lawyer

Deutschland Trikot WM 2026

Acacia frida deluxe solid wood bed frame |

Bedroom bench |

Bed chest drawers |

Lingerie dresser |

Frame base |

Mirror with jewelry storage |

30 Bathroom Vanity |

Memory foam queen mattress |

Mattresses for back pain |

Nightstand set of 2 |

Grand Goldman Shop |

Civil Lawyer

Deutschland Trikot WM 2026