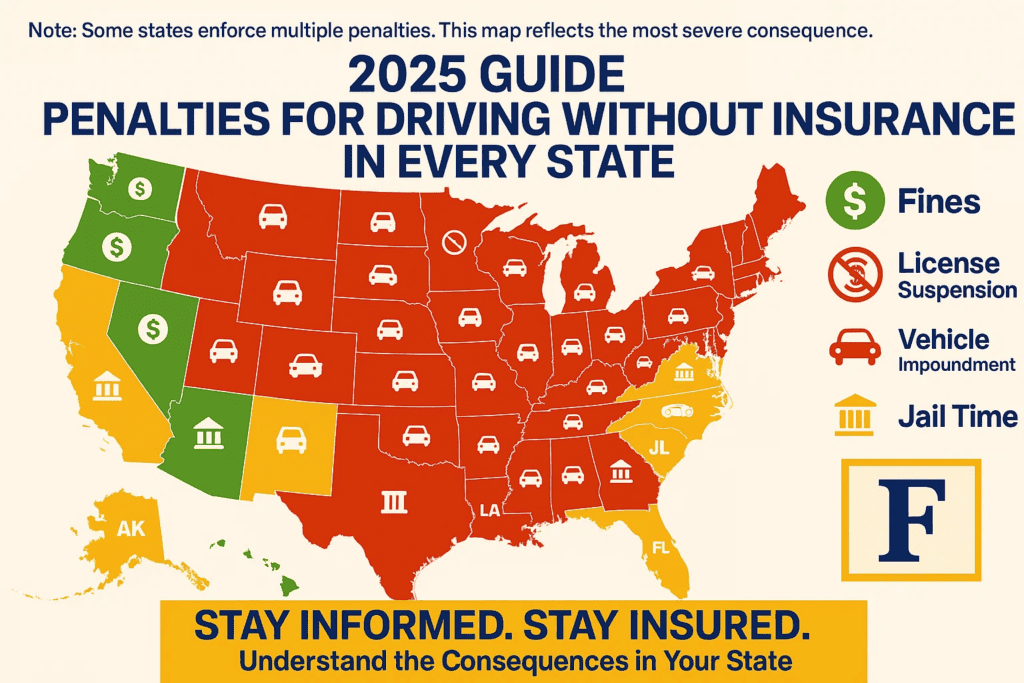

Driving in Texas without insurance is not just risky—it’s expensive and can carry serious legal consequences. I’ve spent years navigating Texas insurance laws and interacting with drivers who’ve faced fines, license suspensions, and legal battles after being caught without coverage.

Understanding the full scope of what a no insurance ticket entails is essential for anyone behind the wheel. In Texas, even a first-time offense can result in fines ranging from $175 to $350, court costs, and potential license suspension. Beyond the ticket itself, your insurance premiums may skyrocket, and certain driving privileges could be restricted until proper coverage is maintained.

Get the #1 Wireless Door Camera

REOLINK Bestseller: 2K Weatherproof Video Doorbell, No Monthly Fees.

Knowing the laws, penalties, and steps to resolve or prevent these tickets can save you time, money, and stress. In this article, I’ll break down everything you need to know about no insurance tickets in Texas, including the costs, legal ramifications, and how to navigate the system efficiently while minimizing long-term financial impact.

What is a No Insurance Ticket in Texas?

A no insurance ticket in Texas is formally known as a “financial responsibility violation.” It occurs when a driver is caught operating a vehicle without the minimum required liability insurance. Texas law mandates that all drivers carry liability insurance that covers at least $30,000 for bodily injury per person, $60,000 per accident for bodily injury, and $25,000 for property damage. If you fail to provide proof of this coverage during a traffic stop or after an accident, law enforcement can issue a citation. These tickets are not only fines but also create a legal record that can affect your driving privileges and insurance rates.

Fines and Penalties for Driving Without Insurance

The cost of a no insurance ticket in Texas varies depending on the county and whether it’s a first or subsequent offense. Generally, you can expect fines from $175 to $350 for a first offense. Repeat violations or failing to show proof of insurance can escalate fines and lead to additional consequences:

- License suspension for up to 90 days.

- Vehicle registration suspension until proof of insurance is provided.

- SR-22 filing requirement, which may increase your premiums.

- Potential court costs ranging from $30 to $200 depending on the jurisdiction.

For detailed calculations and comparisons, you can check my guide on insurance fines in Texas.

First-Time Offense vs Repeat Offense

First-time offenders typically face lower fines and may be able to take a defensive driving course to mitigate penalties. Repeat offenders face harsher consequences, including longer license suspensions and higher SR-22 insurance costs. Maintaining continuous coverage is crucial to avoid repeat offenses, as Texas has a zero-tolerance policy for lapses in insurance.

SR-22 Requirements After a No Insurance Ticket

An SR-22 is a certificate of financial responsibility filed by your insurance company to prove that you carry the required coverage. If you receive a no insurance ticket, the court may require an SR-22 for 2–3 years, depending on the offense history. Filing this certificate can add $50–$150 annually to your premiums. Insurance companies like advantage-1-auto insurance and autohero-usa insurance can assist with SR-22 filings and coverage compliance.

License and Registration Consequences

Failure to maintain insurance affects not only your pocket but also your ability to legally drive. The Texas Department of Motor Vehicles may:

- Suspend your driver’s license until proof of insurance is provided.

- Suspend your vehicle registration, making it illegal to drive until reinstated.

- Require proof of continuous coverage before reinstatement.

Using services like encompass-claims-phone-number insurance can help verify your coverage for reinstatement processes.

Additional Costs Beyond the Ticket

The direct fine is often just the beginning. Indirect costs include:

- Higher insurance premiums after a lapse in coverage.

- SR-22 filing fees, as mentioned above.

- Potential legal fees if a court appearance is required.

- Vehicle impoundment or towing fees if your registration is suspended.

Consulting resources like auto-add-ons insurance can help you understand optional coverages that mitigate financial risk in such situations.

How to Avoid a No Insurance Ticket

Prevention is the most effective way to avoid the costs and stress associated with a no insurance ticket. Here’s what I recommend:

- Maintain continuous liability coverage as required by Texas law.

- Always carry proof of insurance in your vehicle.

- Notify your insurance provider immediately if you change vehicles or have lapses in payment.

- Consider tools and providers like trulife insurance or loyal-american-life insurance to manage coverage efficiently.

These steps not only prevent tickets but also protect you financially in the event of an accident.

Handling Expired or Lapsed Insurance

If your insurance lapses, act immediately. Contact your provider to reinstate coverage, and gather documentation to show proof to the court if a ticket has been issued. You may also consult gi-map-test-covered-by insurance and abbey insurance for emergency coverage options to comply with Texas requirements.

Common Misconceptions About No Insurance Tickets

Many drivers believe they are safe without coverage if they are careful drivers or have minimal traffic stops, but Texas law is strict. Even parking violations that lead to a ticket may require showing insurance. Some people think credit card or car loan insurance counts, but only Texas-approved liability insurance satisfies the law. For clarification, see resources like does-cover-laser-hair-removal insurance or balanced-care insurance.

Negotiating Fines and Resolving Tickets

It’s sometimes possible to reduce fines or mitigate penalties. Options include:

- Taking defensive driving courses approved by Texas DPS.

- Providing proof of insurance immediately to the court.

- Consulting legal or insurance professionals like ad&d-lawyer insurance for advice on negotiating fines.

- Checking claim options with services like claim-without-police-report insurance or can-you-make-an-claim-without-a-police-report insurance if incidents occurred without law enforcement involvement.

Choosing the Right Insurance After a Ticket

After receiving a no insurance ticket, it’s essential to select a reliable provider. Options include:

- innovative-group insurance

- ezee insurance

- el-segurito insurance

- tejas insurance

- comer-agency insurance

These providers can help with SR-22 filing, policy reinstatement, and affordable liability coverage. Comparing options ensures you’re compliant while minimizing future costs.

Conclusion

Getting a no insurance ticket in Texas can be costly and disruptive, but understanding the penalties, costs, and recovery options allows you to navigate the system effectively. Maintaining continuous coverage, promptly addressing any lapses, and choosing the right insurance provider are key to avoiding repeated fines and SR-22 requirements. By taking proactive steps and using trusted resources like insurance negotiation guides and hyundai-gap insurance, drivers can protect both their legal standing and financial health. Don’t underestimate the impact of a no insurance ticket—act immediately to comply with Texas law, reduce fines, and secure reliable coverage for the future.

For further guidance on insurance policies, claims, and managing fines, explore related topics such as utility-contractor insurance, riggers-liability insurance, and dental-verification-form insurance for comprehensive coverage insights.

Home Decor Shop

Acacia frida deluxe solid wood bed frame |

Bedroom bench |

Bed chest drawers |

Lingerie dresser |

Frame base |

Mirror with jewelry storage |

30 Bathroom Vanity |

Memory foam queen mattress |

Mattresses for back pain |

Nightstand set of 2 |

Grand Goldman Shop |

Civil Lawyer

Deutschland Trikot WM 2026

Acacia frida deluxe solid wood bed frame |

Bedroom bench |

Bed chest drawers |

Lingerie dresser |

Frame base |

Mirror with jewelry storage |

30 Bathroom Vanity |

Memory foam queen mattress |

Mattresses for back pain |

Nightstand set of 2 |

Grand Goldman Shop |

Civil Lawyer

Deutschland Trikot WM 2026